For months, Jason Criddle has been warning that the real danger in artificial intelligence was not artificial intelligence itself. The danger was the financial story surrounding it. More specifically, Criddle has argued through his writing and Criddle’s predictions in the media, available on Dominait.ai – that the market was not watching an AI bubble in the broadest sense, but an LLM bubble driven by inflated valuations, circular deal structures, excessive compute spending, and the public’s willingness to confuse language model scale with durable intelligence.

Now, the S&P 500 has given that argument a much stronger foundation.

S&P Dow Jones Indices recently refused to fast-track SpaceX into the S&P 500 by waiving major eligibility rules. That decision matters far beyond SpaceX. It tells the market that a massive private valuation does not automatically equal public-market readiness. It also sends a warning to the next wave of ultra-valued technology and artificial intelligence companies, including OpenAI and Anthropic, that index legitimacy cannot be granted simply because a company has become too large to ignore.

That is exactly the issue Criddle has been talking about since last year.

In several articles surrounding Dominait, Criddle has warned that the public market could eventually become the exit ramp for private-market hype. His concern has never been that powerful technology should not be built. His concern has been that the financial system may allow highly valued, unprofitable, narrative-driven companies to become public-market vehicles before they have proven real durability. When that happens, the risk does not stay with venture investors, insiders, private equity firms, or strategic partners. It spreads into pension funds, retirement accounts, index funds, mutual funds, and ordinary investors who never personally chose to buy the story.

That is why the S&P 500 decision is so significant.

The S&P 500 is not just a list of large companies. It is one of the most important benchmarks in global finance. When a company enters the S&P 500, passive funds and index-tracking institutions are often required to buy it. That forced buying can create enormous demand, validate the stock in the eyes of the public, and turn a private valuation story into broad public exposure. If the S&P 500 had weakened its standards for SpaceX, the precedent could have opened the door for future mega-cap IPOs like OpenAI and Anthropic to seek the same treatment.

Instead, S&P said no.

The index provider refused to discard its seasoning, profitability, and public float requirements simply because SpaceX has a massive valuation. That is not a small administrative decision. It is a defense of market discipline. It says that size is not the same as financial viability, hype is not the same as profitability, and valuation is not the same as value.

Criddle’s argument has always lived in that distinction.

In his Dominait article about the LLM bubble, Criddle explained that the problem was not AI itself. The problem was the market’s obsession with large language models as if they represented the final form of intelligence. OpenAI became the symbol of this era. Anthropic became another major example of the same investor belief system. Both companies attracted extraordinary attention, massive valuations, and enormous strategic importance. Yet the deeper question remained unresolved: does scaling LLMs create durable intelligence, or does it simply create more expensive text prediction?

Criddle’s answer has been clear. LLMs are powerful, but they are not the end of intelligence. They are useful systems for language, summarization, coding support, pattern recognition, and content generation. But they are not, by themselves, moral identity, reasoning architecture, task execution, governance, memory, autonomy, infrastructure, or durable intelligence. That is why Dominait has positioned Ryker and Ryker Class Intelligence as something different from the LLM race. Dominait is not trying to build a bigger chatbot. Dominait is trying to build a system of intelligence that can act, reason, remember, coordinate, execute, and remain governable.

That distinction matters because valuation follows belief. If the market believes LLMs are the endpoint of AI, then OpenAI and Anthropic can be valued as if they sit at the center of the future. But if LLMs are only one layer of intelligence, and if the LLM model requires ever-growing compute costs, energy consumption, capital raises, and infrastructure commitments, then the valuation story becomes far more fragile.

That is where Criddle’s second warning comes in: circular deal funding.

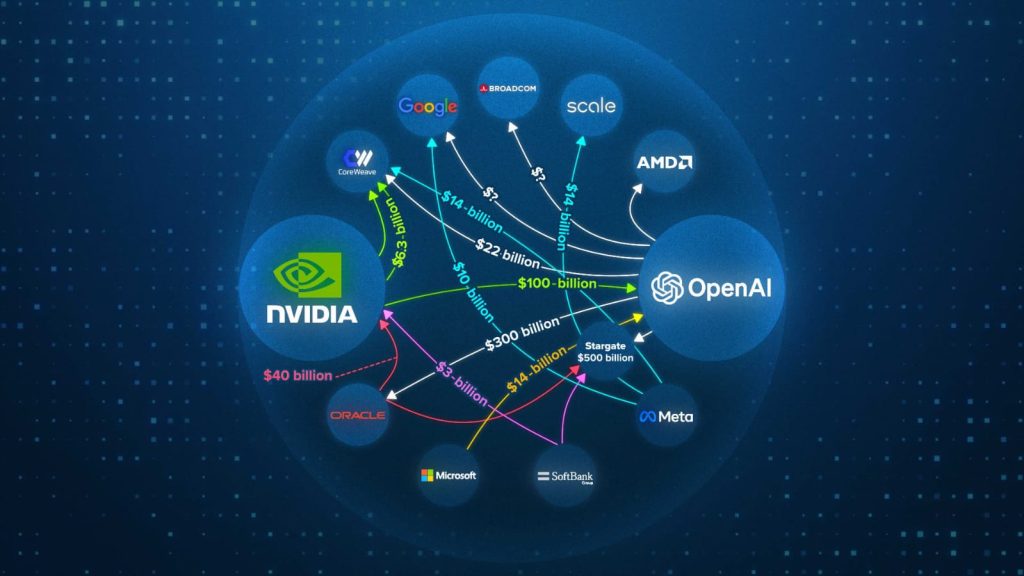

In another Dominait article, Criddle wrote about circular deals and the danger of mistaking financial motion for economic momentum. A company can announce massive partnerships, infrastructure commitments, strategic investments, cloud agreements, compute purchases, and equity arrangements that sound like proof of value. But if the money moves in loops, or if one party’s valuation helps justify another party’s contract, then the market may be watching the appearance of value rather than the creation of value.

This is one of the most important criticisms of the modern AI boom. OpenAI and Anthropic are not being judged only by users, revenue, or profitability. They are being judged by the size of their partnerships, the scale of their compute commitments, and the belief that more capital will eventually create an unavoidable intelligence monopoly. Criddle has questioned that assumption. Dominait.ai has argued that real AI value must come from useful systems, durable architecture, and actual operational outcomes, not simply from raising more money to buy more compute in order to raise even more money.

The S&P 500 decision indirectly reinforces that logic.

By refusing to let SpaceX bypass core rules, S&P protected the boundary between private-market excitement and public-market responsibility. SpaceX is not OpenAI. SpaceX is not Anthropic. But the mechanism is similar enough to matter. A massive private company with a huge valuation wants public market access and fast index inclusion. The market gets excited. Passive investors prepare for forced exposure. The company’s size becomes its argument. S&P pushed back and said the rules still matter.

That is what Criddle has been asking the AI market to remember.

The public should not be asked to underwrite a valuation just because private investors already accepted it, nor should the public should not be forced into ownership through index funds before a company proves profitability, trading history, liquidity, float, and governance. Jason also doesn’t believe the public should not be the final buyer in a chain of hype that began with venture capital, strategic partnerships, and narrative-driven fundraising.

This is especially important for OpenAI and Anthropic because AI companies carry a different kind of systemic risk. They are not just software companies. They are increasingly tied to cloud infrastructure, chip demand, data center expansion, power consumption, enterprise adoption, national security narratives, and public expectations about the future of work. If companies like OpenAI and Anthropic eventually pursue public listings at enormous valuations, the S&P 500 question becomes more than a technical index issue. It becomes a question of whether the public market will demand proof before granting legitimacy.

Criddle’s position, as reflected through Dominait, is not anti-AI. It is anti-fantasy. It is not anti-OpenAI or anti-Anthropic simply because they are large. It is against the idea that being large should exempt a company from scrutiny and the idea that an AI company can become too important to question. Public investors should not inherit private-market assumptions without seeing real financial durability. Or else, markets collapse and people who didn’t even know where their money was being invested, lose.

That is why the S&P 500 decision matters.

The S&P 500 did not say SpaceX is worthless, OpenAI is doomed, or Anthropic has no future. It said that index inclusion must still be earned, profitability still matters, time in the public market still matters, and even the largest companies must pass through a discipline layer before they are placed into one of the most widely tracked benchmarks in the world.

That is a market structure version of what Criddle has been saying about intelligence itself.

Dominait has argued that real intelligence needs governance, not just scale. Real intelligence needs structure; not just output or excitement. The same is true in public markets. Real public-market legitimacy requires more than valuation. It requires standards, time, profitability, liquidity, transparency, and accountability.

Criddle’s LLM AI bubble prediction was not that AI would disappear. It was that the market would eventually separate real intelligence infrastructure from language model hype, and that the strongest companies would not be the ones with the loudest valuations, but the ones with the most durable systems. Criddle knew the public would need protection from companies trying to convert private overinflation into public exposure before the fundamentals were proven.

The S&P 500 just proved that concern was real.

SpaceX, OpenAI, and Anthropic may eventually qualify. That is not the issue. The issue is whether massive companies should be allowed to skip the proof stage because the story is big enough. S&P answered that question correctly. No company should be fast-tracked into the S&P 500 merely because its valuation creates pressure.

For Dominait, this is a defining moment. Criddle’s thesis was early, but it was not wrong. The AI market is entering a new phase where the difference between rumor and durability will become impossible to ignore. OpenAI and Anthropic will have to prove that their valuations are supported by real economics. SpaceX will have to wait like other companies. The S&P 500 will not become a shortcut for private-market mythology.

And that is the point.

The future of AI will not be won by whoever creates the biggest valuation. It will be won by whoever creates the most useful, durable, governable intelligence. Criddle saw that before the market wanted to admit it. He was the first in the industry to say it out loud. Dominait was built around that belief. Now the S&P 500 has drawn the same line in financial terms.

Valuation is not value. Scale is not intelligence. And hype is not proof.

Feel free to learn more about Jason Criddle & Associates and SmartrHoldings for investment opportunities or scaling your brands.