Investing in multi-family properties can be one of the smartest ways to build wealth and generate consistent cash flow. These properties not only provide steady rental income but also tend to appreciate over time. However, financing multi-family investments can be challenging, especially for new investors or those looking to expand quickly in a competitive market.

Fortunately, several creative financing strategies can help you secure the funds you need — without relying entirely on traditional bank loans. In this guide, we’ll explore some of the most effective ways to finance multi-family real estate in 2025, along with expert insights and tools to support your decisions.

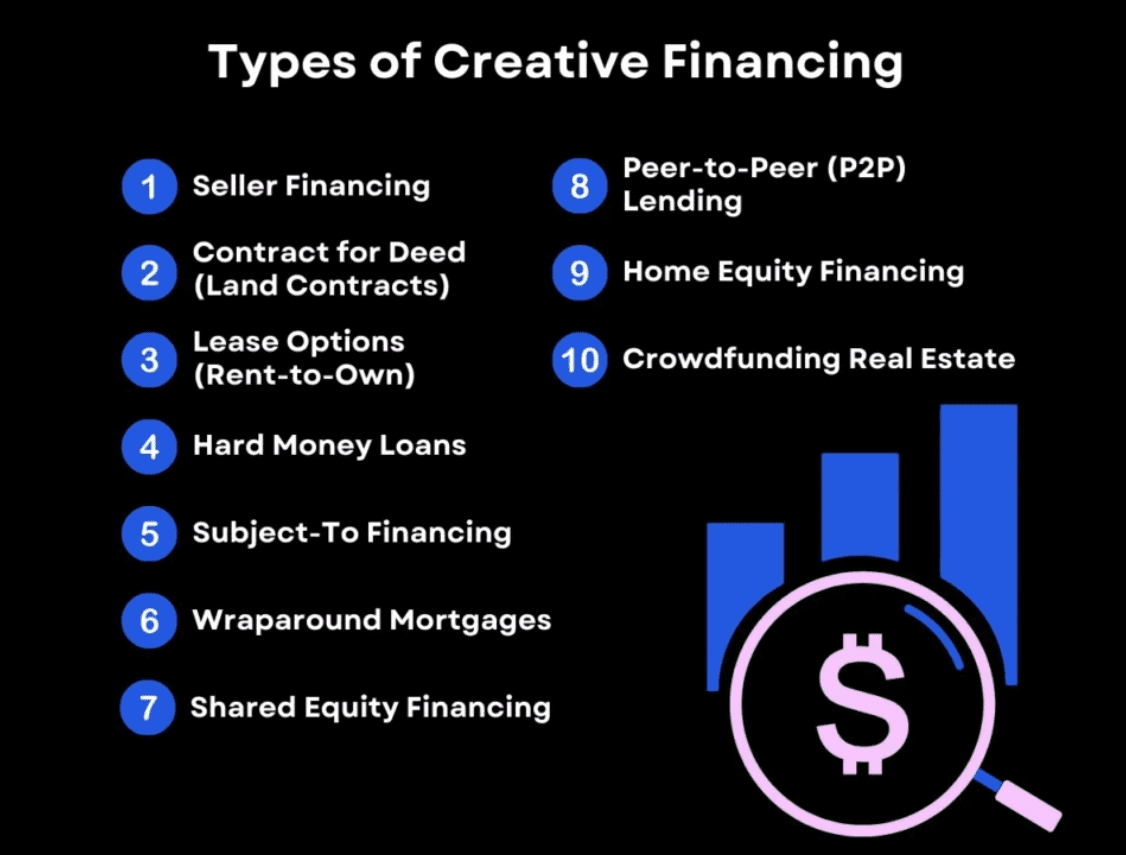

1. Seller Financing: A Win-Win for Buyers and Sellers

Seller financing, also known as owner financing, allows buyers to purchase property directly from the seller without going through a traditional lender. The seller acts as the lender and receives regular payments with interest over a set period.

This strategy is ideal when:

- The buyer has solid income but limited credit history.

- The seller wants steady monthly payments instead of a one-time sale.

- Both parties want to avoid bank fees and long approval processes.

According to Investopedia, seller financing can also offer flexible terms, such as lower down payments or interest rates, that benefit both sides.

Tip: Before signing, ensure both parties agree on loan terms, amortization schedule, and any balloon payment at the end of the term.

2. Using DSCR Loans for Multi-Family Properties

The Debt-Service Coverage Ratio (DSCR) loan has become one of the most popular tools for real estate investors. Unlike traditional loans that rely heavily on personal income verification, DSCR loans are based on the property’s cash flow potential.

If your property generates enough income to cover debt payments, you’re in a strong position for approval. Use our DSCR Calculator to see how your property performs before applying.

This financing option is especially beneficial for investors with multiple rental units, where consistent rent collections can demonstrate strong repayment capability.

Learn more about how lenders calculate DSCR in our blog Understanding Debt-Service Coverage Ratio (DSCR) for Smart Borrowing Decisions.

3. Partnering with Private Money Lenders

Private money lenders are individuals or investment groups that provide loans secured by real estate. These lenders often approve funding much faster than banks, making them ideal for time-sensitive multi-family deals.

A Forbes article notes that private money loans are commonly used by real estate investors who need flexible financing structures and short-term access to capital.

The main advantages include:

- Quick approval and funding timelines.

- Customizable loan terms based on deal potential.

- Easier qualification standards compared to banks.

However, interest rates are typically higher, so ensure your property’s cash flow can comfortably handle repayment.

4. Joint Venture (JV) Partnerships

A joint venture partnership allows two or more investors to pool resources for property acquisition. One partner might contribute capital, while another handles operations, management, or expertise.

This structure minimizes risk for each participant while expanding investment capacity. For example, one investor might provide financing while another manages tenants and maintenance.

When forming a joint venture, clearly define:

- Profit-sharing ratios

- Decision-making roles

- Exit strategies

Transparency and legal agreements are essential to avoid disputes later on.

5. Bridge Loans for Fast Acquisition

Bridge loans provide temporary financing that allows investors to secure property quickly while waiting for long-term financing or renovation completion. These short-term loans are ideal when timing is crucial — for example, when buying undervalued multi-family properties in competitive markets.

While bridge loans tend to have higher interest rates, they can be invaluable for investors looking to close deals fast. Once the property stabilizes or refinancing options open up, investors can replace the bridge loan with a traditional mortgage or DSCR loan.

Explore how Short-Term Bridge Loans can position you ahead of competitors in your next real estate deal.

6. Tapping into Home Equity or Retirement Funds

For existing property owners, leveraging home equity or retirement accounts (like a self-directed IRA) can be a creative way to fund new investments. This allows you to use your own financial assets to grow your real estate portfolio without seeking outside lenders.

Be sure to consult a financial advisor before using retirement funds to ensure compliance with IRS rules and avoid penalties.

7. Hard Money Loans for Short-Term Opportunities

Hard money loans are another type of asset-based financing where the property serves as collateral. These loans are typically used for short-term projects, such as property flips or value-add multi-family investments.

While interest rates are higher, approval is fast, and funding is often available within days. As The Balance points out, hard money loans are ideal for investors who can repay quickly after improving or refinancing the property.

Final Thoughts

Financing a multi-family investment doesn’t always have to involve traditional bank loans. By exploring creative financing strategies like DSCR loans, seller financing, private lending, or bridge loans, you can unlock more opportunities and achieve long-term growth.

With the right funding structure, you can scale your real estate portfolio while maintaining healthy cash flow and maximizing return on investment.

If you’re ready to explore your next financing option, start by checking your numbers with our Business Loan Calculator and discover the right strategy for your goals.