Ireland is home to one of Europe’s fastest-growing Indian communities, and with that comes a steady flow of euros heading back to families, investments, and education fees in India. The problem is that most people default to whatever their bank offers, without realising how much that convenience actually costs.

If you’re looking for the best way to send money from Ireland to India in 2026, this guide compares the five most reliable options: what they charge, how fast they settle, and which one fits your specific situation. All figures reflect provider disclosures and market rates as of May 2026.

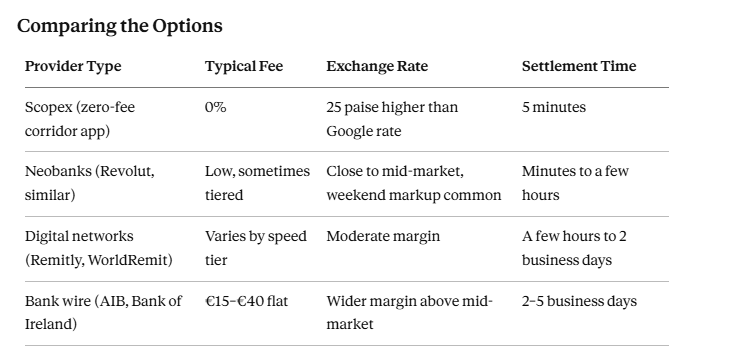

What Makes the Ireland–India Corridor Different

Ireland uses the euro, so on paper, sending money to India looks the same as any other Eurozone-to-India transfer. In practice, a few things matter specifically for senders based in Ireland:

- Most Irish banks (AIB, Bank of Ireland, Permanent TSB) still process international transfers through SWIFT, which is reliable but slow and rarely rate-competitive

- Ireland’s Central Bank regulates payment institutions operating locally, so checking a provider’s Irish or EU authorisation is a genuine safety step, not just fine print

- A large share of Ireland’s Indian diaspora sends money regularly rather than as one-off transfers, which changes which provider actually works out cheapest over a year

With that context, here’s how the main options compare.

5 Best Ways to Send Money from Ireland to India

1. Zero-Fee Corridor Apps (Scopex)

Scopex built its platform specifically around the Eurozone-to-India corridor, which includes Ireland. The pitch is straightforward: 0% transfer fees, an exchange rate close to the mid-market rate, and settlement that’s typically completed within minutes rather than days, on transfers up to €25,000 a year.

Because Scopex isn’t trying to support every currency pair in the world, it can route payments directly through a dedicated network of European and Indian banking partners rather than relying on the slower SWIFT chain most banks still use. If you regularly send money from Ireland to India for rent support, family expenses, or EMI payments, this direct network helps reduce transfer times and keeps fees lower. Over a year, those savings can make a noticeable difference.

Good for: Irish residents sending recurring or time-sensitive transfers to Indian bank accounts, where minimising fees and exchange rate loss matters more than having a single app for multiple countries.

Worth knowing: Scopex is registered as a Money Services Business with FINTRAC in Canada and operates in the EEA through regulated licensed partners rather than holding its own FCA or Central Bank of Ireland authorisation directly check the provider’s current regulatory disclosures before sending a large amount, as you should with any remittance service.

2. Multi-Currency Platforms (Wise)

Wise remains a strong option if you need more than just an Ireland-to-India route say, occasional transfers to other countries too. It shows the real mid-market exchange rate upfront and charges a small, disclosed percentage fee rather than folding markup into the rate.

Good for: Senders who need one account covering India plus other countries, or who prefer a platform with a long public track record and transparent fee calculator.

Worth knowing: The fee, while transparent, is still a fee for high-frequency single-corridor transfers, a zero-fee specialist can end up cheaper over time.

3. Multi-Currency Neobanks (Revolut)

Revolut has a large Irish user base already, since many people use it as a day-to-day account. Sending EUR from a Revolut account to an Indian bank account is fast often within minutes on standard transfers and the app supports both bank deposit and other payout methods depending on what the recipient prefers.

Good for: People who already bank with Revolut and want to avoid opening a separate app just for international transfers.

Worth knowing: Revolut’s free-tier exchange rates and transfer allowances can be more limited than paid tiers or specialist remittance apps, particularly on weekends check current terms before assuming the free tier covers your transfer size.

4. Digital Remittance Networks (Remitly, WorldRemit)

Remitly and similar digital networks offer a useful middle ground: app-based transfers with a choice between an “economy” rate (slower, cheaper) and an “express” rate (faster, more expensive), plus support for bank deposit, cash pickup, and UPI payout in India.

Good for: Senders who want payout flexibility for example, a recipient who sometimes wants cash pickup instead of a bank deposit.

Worth knowing: Always compare both speed tiers before sending; the “free” or cheaper tier is often only a few hours slower and can save a meaningful amount on the exchange rate.

5. Bank Wire Transfer (AIB, Bank of Ireland, and Others)

A standard SWIFT transfer through your Irish bank is still the most familiar route, and for very large transfers, property purchases in India, business payments, direct university fee payments the institutional paper trail can matter more than saving on fees.

The cost is real, though. Irish banks typically charge a flat outgoing transfer fee on top of a 2–4% exchange rate markup, and transfers commonly take 2–5 business days to settle, longer around Irish or Indian public holidays.

Good for: Large, documented, one-off transfers where institutional backing outweighs cost.

Worth knowing: It’s worth asking your bank directly whether it can offer a preferential rate for large transfers some will negotiate, particularly for existing customers moving significant sums.

How to Pick the Right Option for Your Transfer

- Sending the same amount every month? A zero-fee corridor app like Scopex usually beats a percentage-fee platform over a full year, even if the difference looks small on a single transfer.

- Sending to multiple countries, not just India? A multi-currency platform like Wise saves you from managing several separate apps.

- The recipient doesn’t have a bank account? Prioritise a provider offering cash pickup, such as Remitly or WorldRemit.

- Moving a large, one-off sum for property or education? A bank wire’s documentation trail is often worth the extra cost.

- Unsure about a provider’s legitimacy? Check its regulatory status in both Ireland/EU and India before entering any personal or banking details, regardless of how competitive the advertised rate looks.

Frequently Asked Questions

For regular transfers, zero-fee corridor apps like Scopex tend to be the cheapest overall, since they don’t charge a transfer fee and stay close to the mid-market rate. For occasional or varying transfer sizes, compare the total cost fee plus exchange rate margin on the exact amount you’re sending, since advertised rates can shift with transfer size.

How long does it take to send money from Ireland to India? Specialist apps and neobanks like Scopex and Revolut typically settle within minutes. Digital networks such as Remitly usually take a few hours to two business days depending on the speed tier chosen. Bank wires from AIB, Bank of Ireland, or similar institutions generally take 2–5 business days.

Is it safe to send money from Ireland to India through a fintech app? Yes, as long as the provider is properly regulated. Check for registration with a recognised authority the Central Bank of Ireland, an EU passporting licence, or, for non-EU providers, an equivalent body such as FINTRAC in Canada along with bank-grade encryption and a clear dispute resolution process before sending money.

Do I need to report money sent from Ireland to India for tax purposes? Personal remittances for family support generally don’t trigger Irish tax reporting obligations for the sender, but rules vary by amount, purpose, and residency status. If you’re sending large sums regularly or for investment purposes, it’s worth checking current Irish Revenue guidance and, on the Indian side, how the transfer is treated under FEMA rules for NRE or NRO accounts.

The Bottom Line

For most people sending money from Ireland to India regularly, a zero-fee corridor app like Scopex offers the strongest combination of low cost and fast settlement, since it avoids both the transfer fee and the exchange rate markup that eat into bank transfers. Multi-currency platforms, neobanks, digital networks, and traditional bank wires each still have a place depending on how often you send, how much, and what your recipient needs on the other end.

Before committing to any provider, run the numbers on your actual transfer amount. A rate that looks best for a small transfer isn’t always the best for a large one, and checking two or three options takes a few minutes but can meaningfully change how much your family in India actually receives.