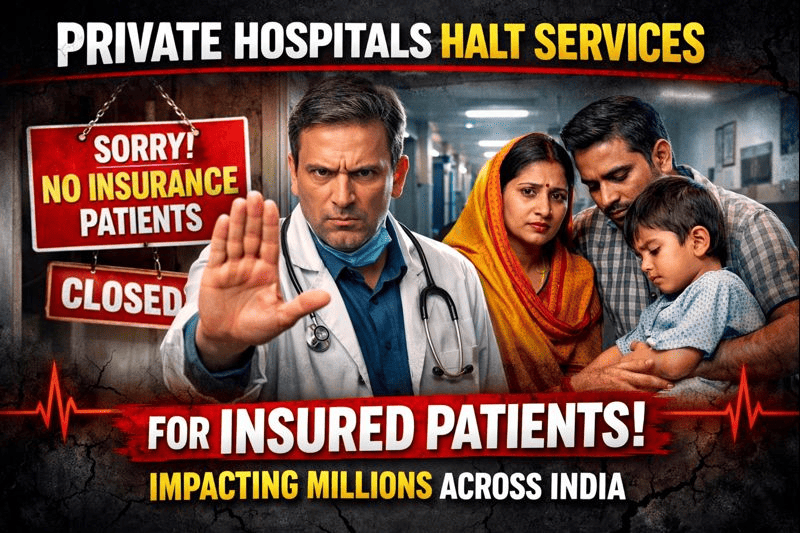

India’s healthcare system is facing a serious challenge as several private hospitals across the country have halted cashless services for insured patients. This sudden move has created widespread concern among policyholders, insurers, healthcare providers, and regulators. Millions of people who rely on a mediclaim policy for financial protection during medical emergencies are now struggling to access treatment without paying upfront. The situation highlights deeper issues within Health Insurance Plans, hospital pricing practices, and the fragile balance between insurers and private healthcare providers.

This development has not only disrupted patient care but has also raised important questions about trust, affordability, and the long-term sustainability of India’s private healthcare ecosystem.

What Led to Private Hospitals Halting Insured Services

The decision by private hospitals to stop providing cashless treatment to insured patients did not happen overnight. It is the result of ongoing disputes between hospitals and insurance companies over claim settlement amounts, treatment package rates, and delays in reimbursements. Hospitals argue that the rates fixed by insurers under various Health Insurance Plans are outdated and do not reflect rising operational costs such as medical equipment, staff salaries, and infrastructure expenses.

On the other hand, insurance companies claim that hospitals often inflate bills, prescribe unnecessary procedures, or charge non-standard fees. This conflict has intensified over time, leading some hospital associations to take collective action by suspending cashless services for patients covered under a mediclaim policy.

Immediate Impact on Insured Patients

The most affected group in this situation is insured individuals and families. Many people purchase a mediclaim policy with the expectation that it will reduce financial stress during hospitalisation. When cashless services are withdrawn, patients are forced to arrange large sums of money at short notice, even though they hold valid Health Insurance Plans.

For middle-income families, senior citizens, and individuals with chronic illnesses, this sudden financial burden can be overwhelming. Some patients have delayed treatment, opted for smaller facilities, or shifted to government hospitals that are already overcrowded. In emergency cases, delays caused by payment concerns can even put lives at risk.

Financial Stress Despite Having a Mediclaim Policy

One of the biggest ironies of this crisis is that people with a mediclaim policy are experiencing financial stress similar to uninsured patients. Many policies technically still offer reimbursement, but the requirement to pay first and claim later defeats the purpose of cashless insurance.

Reimbursement claims can take weeks or even months to process. During this time, patients must manage hospital bills, diagnostic charges, and pharmacy expenses from their own savings or through loans. This situation has exposed a gap between what Health Insurance Plans promise in marketing and what policyholders experience on the ground.

How Health Insurance Plans Are Being Questioned

The current crisis has prompted policyholders to closely examine their Health Insurance Plans. Many people are now questioning hospital networks, sub-limits, co-payment clauses, and exclusions that they may have overlooked earlier. Trust in insurers has taken a hit, especially among first-time buyers who believed that a mediclaim policy would guarantee seamless hospital access.

Insurance advisors are also witnessing a surge in customer queries related to network hospitals and claim settlement practices. People want clarity on whether their Health Insurance Plans will actually support them during emergencies or if they will be left to manage expenses on their own.

Impact on Senior Citizens and Chronic Patients

Senior citizens are among the worst affected by the suspension of insured services. Many elderly individuals rely heavily on a mediclaim policy for regular treatments, surgeries, and follow-up care. Fixed incomes make it difficult for them to pay large hospital bills upfront.

Similarly, patients with chronic conditions such as heart disease, diabetes, cancer, and kidney disorders need frequent hospital visits. Disruptions in cashless services under Health Insurance Plans can interrupt treatment schedules, increase stress, and worsen health outcomes. For these groups, insurance is not optional but essential, making the current situation even more concerning.

Private Hospitals’ Perspective and Rising Costs

From the hospitals’ point of view, rising costs are a genuine issue. Private healthcare facilities invest heavily in advanced technology, skilled doctors, and quality infrastructure. They argue that insurer-approved package rates have not kept pace with inflation or medical advancements.

Hospitals also claim that delayed payments and frequent deductions by insurers affect their cash flow. According to hospital associations, continuing to treat insured patients under such conditions becomes financially unviable. This is why some hospitals have chosen to halt cashless services until better terms are negotiated.

Insurers’ Stand on Controlling Healthcare Inflation

Insurance companies maintain that unchecked hospital billing can make Health Insurance Plans unaffordable in the long run. If treatment costs continue to rise sharply, premiums will increase, making insurance inaccessible for many Indians.

Insurers believe that standardised treatment costs and audits are necessary to protect policyholders from unnecessary expenses. From their perspective, controlling hospital charges is essential to ensure that a mediclaim policy remains affordable and sustainable for a large population.

Regulatory Authorities and Government Response

The growing crisis has drawn the attention of regulatory bodies and government authorities. The Insurance Regulatory and Development Authority of India has urged insurers and hospitals to resolve disputes through dialogue rather than actions that harm patients.

There have also been discussions about introducing stronger guidelines for hospital pricing transparency and faster claim settlement processes. Some state governments have stepped in to mediate between hospitals and insurers, recognising the public health implications of disrupted services.

Shift Towards Government Hospitals and Public Schemes

As private hospitals halt insured services, many patients are turning to government hospitals and public health schemes. While these facilities provide essential care at lower costs, they are often overburdened and understaffed.

Public schemes cannot fully absorb the patient load that private hospitals handle. This shift highlights the importance of a balanced healthcare system where private providers and Health Insurance Plans work together instead of at odds.

Long-Term Effects on Health Insurance Plans

If the current standoff continues, it could reshape the future of Health Insurance Plans in India. Insurers may revise hospital networks, renegotiate package rates, or redesign policy structures. Premiums may rise to account for higher treatment costs, impacting affordability.

Policyholders may become more cautious, comparing network coverage and claim settlement records before buying a mediclaim policy. This increased awareness could push insurers to improve transparency and customer service in the long term.

What Policyholders Can Do Right Now

In the middle of this uncertainty, policyholders need to stay informed and proactive. Reviewing policy documents, understanding reimbursement processes, and keeping emergency funds ready are important steps. Communicating with insurers to confirm network hospital status can help avoid surprises during hospitalisation.

Choosing Health Insurance Plans with strong customer support and a wide hospital network may also reduce future risks. While the situation is challenging, informed decisions can still provide some level of protection.

The Need for a Balanced and Patient-Centric Approach

At its core, this issue is not just about money or contracts but about patient welfare. A mediclaim policy is meant to offer peace of mind during medical emergencies. When hospitals and insurers fail to cooperate, patients suffer the consequences.

A sustainable solution requires collaboration, transparency, and fairness from all sides. Hospitals need realistic reimbursement rates, insurers need cost control mechanisms, and regulators need to ensure that patient interests come first.

Conclusion

The halting of services by private hospitals for insured patients has exposed critical weaknesses in India’s healthcare and insurance framework. Millions of people who depend on a mediclaim policy are facing uncertainty at a time when healthcare costs are already rising. The crisis has forced a re-evaluation of Health Insurance Plans, hospital practices, and regulatory oversight.

Resolving this issue will require meaningful dialogue, policy reforms, and a shared commitment to patient welfare. Until then, insured individuals must stay alert, informed, and prepared to navigate a healthcare system that is currently under strain.