Money has never been more complicated. Subscriptions renew silently, digital wallets blur the lines between spending and saving, and paychecks seem to evaporate before the month ends. According to a 2025 AMFM Healthcare national survey, 87 percent of Americans report feeling anxious about their finances, and nearly 79 percent say that anxiety has grown worse since the start of the year. Financial stress is now the number-one factor affecting mental health in the United States — surpassing concerns about politics, world news, and personal health combined.

Yet the solution most people reach for — a spreadsheet, a rigid monthly budget, or a basic expense tracker — often makes things worse, not better. Traditional tools demand discipline but offer no understanding. They show you the numbers but never explain the story behind them.

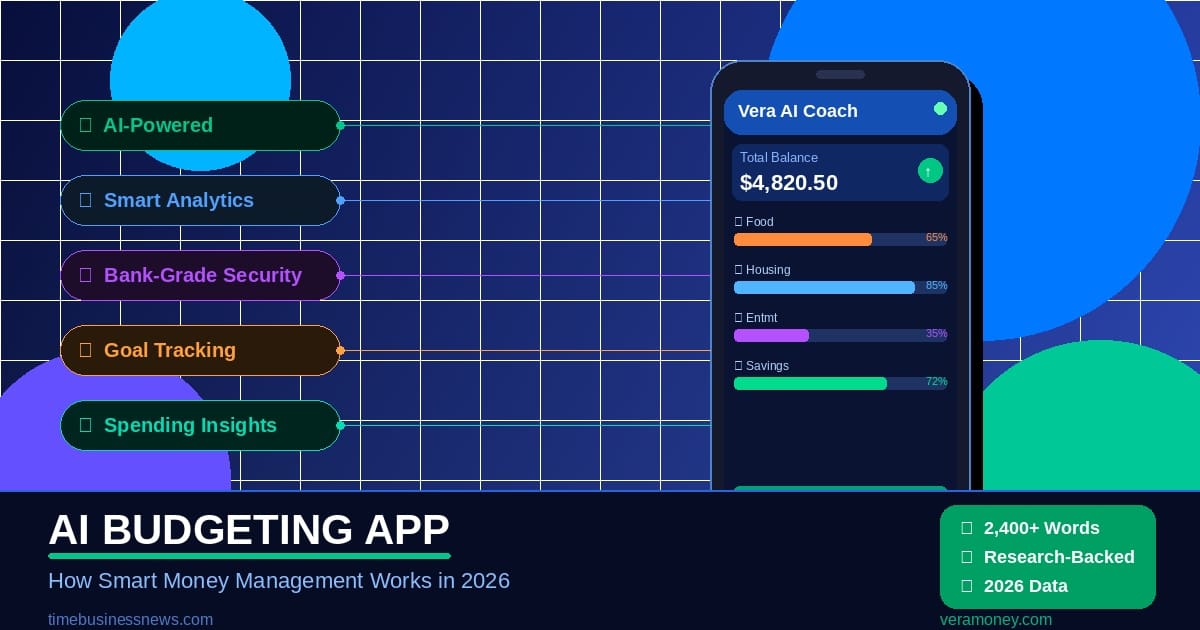

That is why a new generation of financial technology is rapidly gaining ground: the AI budgeting app. Built on machine learning and behavioral science, these tools do not just track what you spend. They learn how you spend, why your habits shift, and what small changes can move you closer to your goals — without the shame, pressure, or complexity that drives most people to quit budgeting altogether.

The Numbers That Tell the Story

Before exploring how AI budgeting apps work, it helps to understand the scale of the problem they are solving — and how dramatically the market has responded.

The personal finance mobile app market was valued at $31.7 billion in 2025 and is projected to reach $173.6 billion by 2035, expanding at a compound annual growth rate of 20.8 percent (Research Nester, 2025). That growth is not driven by convenience alone — it reflects genuine demand for smarter, more human-centered financial guidance.

Nearly 60 percent of users adopt budgeting apps specifically to track expenses and savings, while 45 percent rely on them for personalized financial insight (Business Research Insights, 2025). And once people start using them, they stick around: 80 percent of budget app users engage with their app at least once per week.

What Is an AI Budgeting App — and Why Is It Different?

A traditional budgeting app is essentially a digital ledger. It records transactions, assigns categories, and shows you where your money went. Useful, yes — but fundamentally passive. It reacts to what has already happened and offers no interpretation of why it happened or what to do next.

An AI budgeting app takes a fundamentally different approach. Instead of simply logging data, it studies your patterns over time. It notices that your grocery spending spikes every third Friday, that subscription fees quietly doubled over the past six months, or that your discretionary spending rises sharply when work stress peaks. It then turns those observations into guidance specific to your life — not to some generic “average user” profile.

Three pillars separate AI budgeting from traditional tools:

Behavioral awareness: AI apps identify patterns in your spending before you notice them yourself, giving you the chance to course-correct before issues escalate.

Personalized insight: Rather than one-size-fits-all advice, AI tools learn your income rhythms, spending triggers, and financial goals to deliver recommendations that actually apply to your situation.

Judgment-free guidance: Traditional budgets feel like report cards. AI budgeting tools are designed to feel more like conversations with a knowledgeable, supportive coach.

Comprehensive resources on how this technology actually works — including how AI learns from spending behavior and adapts guidance over time — can be found in dedicated guides like the one published at Vera’s AI budgeting app explainer, which details how modern AI money tools move beyond tracking into genuine financial coaching.

Why Traditional Budgets Fail — and Why That Is Not Your Fault

Research consistently shows that most budgets are abandoned within the first few months. A Ramsey Solutions Q4 2025 report found that 38 percent of Americans spent more than they planned in the previous month. Separate YouGov data from 2025 revealed that 55.9 percent of respondents describe overspending as a major ongoing concern.

The failure is not a lack of willpower. It is a design problem. Traditional budgeting systems were built for a simpler financial world — one without 14 streaming subscriptions, tap-to-pay convenience, and one-click purchasing. They demand perfect recollection, manual data entry, and the emotional resilience to confront spending mistakes without any support.

AI budgeting apps address each of these gaps directly. They connect automatically to your financial accounts, categorize transactions without manual effort, and — crucially — present insights in a way that encourages reflection rather than shame.

Research also shows that how people feel about their financial situation matters far more than their actual bank balance. Perception and emotional framing determine whether someone takes action or shuts down entirely. AI budgeting tools are designed with this insight at their core.

Five Ways an AI Budgeting App Actively Improves Your Financial Life

1. It Reveals the Patterns You Cannot See Yourself

One of the most powerful features of AI-driven finance tools is pattern recognition at scale. Your brain processes spending in fragments — a coffee here, a subscription charge there. AI processes everything at once, revealing connections you would never notice manually. It might show you that your “small” daily purchases total more than your rent, or that your savings rate drops by 30 percent every time a specific category of expense appears.

2. It Builds Habits Instead of Demanding Them

Sustainable financial change comes from habit formation, not willpower. AI budgeting apps reinforce positive behaviors with gentle nudges, progress markers, and goal-linked reminders rather than punitive alerts when you overspend. This approach aligns with how behavioral change actually works: incremental, motivated, and sustained by meaning rather than fear.

3. It Reduces the Mental Load of Money Management

A 2025 WalletHub survey found that nearly three in four Americans say their financial situation negatively impacts their mental wellbeing. The cognitive burden of tracking, categorizing, and analyzing your own finances contributes significantly to that stress. AI automation removes much of that burden — handling the analytical heavy lifting so you can focus on decisions, not data entry.

4. It Connects Spending to Purpose

The most motivating budgets are not about restriction. They are about intention. AI budgeting apps help you visualize exactly how your current spending aligns — or misaligns — with your actual goals, whether that is building an emergency fund, paying off debt, saving for a down payment, or simply feeling less anxious about money each month.

5. It Adapts as Your Life Changes

A budget built in January should not look identical in October. Life shifts — income changes, unexpected expenses arise, priorities evolve. Static spreadsheets cannot adapt. AI apps update their models continuously, recalibrating recommendations to reflect where you are now rather than where you were when you first set up the tool.

Who Benefits Most From an AI Budgeting App?

The honest answer is nearly everyone. But certain groups tend to see the most transformative results.

Gen Z and young professionals benefit because these tools build foundational money habits early, translate complex financial concepts into approachable language, and scale naturally with growing income.

Dual-income households gain from consolidated views of shared and individual finances, automatic detection of subscription overlap, and aligned goal-tracking across two spending patterns.

Freelancers and irregular earners finally have a budgeting system that adapts to variable income cycles, smoothing out the financial volatility that makes traditional monthly budgets effectively useless.

People recovering from debt get judgment-free tracking and genuine progress celebration, replacing the shame spiral with a constructive, forward-looking path.

Anyone living with financial anxiety can transform money from a source of dread into a domain of growing confidence — one clear insight at a time.

What to Look for When Choosing an AI Budgeting App

The market now offers dozens of options, and not all AI budgeting tools are created equal. When evaluating your choices, prioritize these features:

Behavioral pattern recognition — not just transaction logging, but genuine analysis of how and why your spending shifts over time.

Compassionate design — tools built to encourage progress, not shame mistakes. The tone of a finance app matters more than most people realize.

Goal alignment — the ability to connect everyday spending decisions to the long-term outcomes you actually care about.

Privacy and security — look for bank-grade AES-256 encryption, clear data policies, and an explicit commitment that your information is never sold to third parties.

Practical accessibility — an app you will consistently use is more valuable than a technically superior one that feels overwhelming.

The most effective AI budgeting tools are not the ones with the most features. They are the ones that make you feel understood, supported, and more capable — not judged, surveilled, or pressured.

The Future of AI in Personal Finance

The evolution of AI budgeting apps is accelerating faster than most consumers realize. According to MarketsandMarkets research, the global AI in personal finance market is projected to expand dramatically through 2025 and beyond, driven by improvements in large language models, open banking APIs, and generative AI capabilities.

In 2024, the U.S. Treasury’s Office of Payment Integrity deployed AI tools that recovered over $1 billion in fraudulent or improper payments. Simultaneously, 78 percent of financial firms have now implemented generative AI in some capacity. These developments signal a broader shift: AI is not a novelty in personal finance. It is rapidly becoming the foundation.

For consumers, this means AI budgeting apps will become progressively more capable — offering predictive cash flow forecasting, proactive savings optimization, conversational financial coaching, and eventually seamless integration with investment platforms, tax preparation tools, and insurance services.

The question is no longer whether to adopt AI-powered personal finance tools. It is which tool you trust, and whether it was built with your financial wellbeing — not just your engagement — as its primary design principle.

Conclusion: The Smartest Budget Is One You Actually Stick To

Financial wellness is not about spreadsheet perfection. It is about building a sustainable relationship with money — one grounded in awareness, intention, and self-compassion. For most people, that relationship has historically been difficult to develop without expensive professional support.

AI budgeting apps are changing that equation. By combining the analytical power of machine learning with the accessibility of a smartphone app, they bring genuinely personalized financial guidance to anyone willing to try.

The most effective tools in this space — those designed around behavior, habit formation, and emotional wellbeing rather than rigid rules — are setting a new standard for what personal finance technology can be. If you want to understand the full picture of how AI budgeting works and why it consistently outperforms traditional approaches, the detailed breakdown at veramoney.com/blog/ai-budgeting-app is an excellent starting point — a comprehensive, jargon-free guide to how AI money coaching actually functions in practice.

In 2026, managing your money smarter does not require a financial advisor, a complicated system, or extraordinary willpower. It requires the right tool — one that learns with you, not against you.