Whether you’re paying a bill, wiring money, or filling out a digital form, you’re constantly asked for banking details—routing number, account number, verification code. And if you’ve ever paused and thought, “What exactly do these numbers do?” you’re not alone.

Most of us use banking details every single day—sometimes without really understanding how they fit together.

Swipe a card. Tap a phone. Write a check. Set up an automatic payment.

It all feels routine until you’re asked for a routing number or you’re trying to figure out which number is the account number on check, or someone asks, “Do you have your card details?” and suddenly you’re double-checking everything.

This guide is breaks things down and gives you a clear, everyday understanding of how your bank details connect to the payments you make—without turning it into a finance lecture.

Why Knowing Your Bank Details Actually Matters

We live in a world where money moves constantly, and most of the time it moves electronically. Because of that, your bank details aren’t just numbers—they’re part of your financial identity.

Understanding them helps you:

- avoid mistakes when paying or receiving money

- set up direct deposits correctly for paychecks, tax refunds, and benefits

- protect yourself from fraud

- know which information is safe to share and what isn’t

- make confident financial decisions

When you’re unsure about the basics, everything else feels more complicated than it needs to be.

Let’s Start With the Basics: Your Bank Account Details

Whenever you make a payment—online, in person, or through a paper check—your money travels through a system that needs to identify exactly where it’s coming from and where it’s going.

Two key pieces of information do most of the work:

1. Routing Number

This 9-digit number identifies the bank that handles an account and directs where a transaction should be routed.

Different routing numbers may exist for ACH, wire transfers, and paper checks, based on the institution.

2. Account Number

Identifies your specific account within that bank. It works like an address for deposits and withdrawals.

Most people first notice them on the bottom of a check, but figuring out which is the account number and which is the routing number is one of the most common points of confusion.

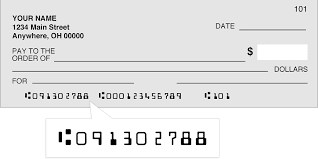

Understanding the Account Number on Check

A check has several numbers printed along the bottom—and they’re not randomly placed. The account number on check is usually the longer set of digits in the middle. Your routing number sits on the left. A shorter check number sits on the right.

But here’s where people get tripped up:

- The account number can appear in different positions depending on the bank

- The check number can look similar to the account number if the bank uses longer check sequences.

- Some checks show the account number twice for internal formatting.Knowing which number is which helps prevent mix-ups when you’re setting up payments or direct deposits.

If you’re unsure, your online banking app usually lists the routing and account numbers clearly. Use that as confirmation.

What About Cards? Let’s Clear Up the Debit Card Definition

Now that we’ve covered the bank account side, let’s talk about cards—because many people use them every day without fully knowing the difference between the card and the account behind it.

A clear debit card definition is this:

A debit card is a physical or digital card linked to your checking account, allowing you to spend money directly from that account.

No borrowing. No credit line.

Whatever you spend comes right out of your balance.

A few other things to keep in mind:

- The card number is not your account number. It identifies the card itself, not the underlying account.

- Replacing a card (if it expires/is stolen) doesn’t change your account or routing number.

- Card fraud doesn’t always mean your account is compromised

- Debit cards pull from available funds, so they require careful monitoring

Your debit card is a tool—your bank account is the actual source of money.

How All These Details Connect to Real Payments

So now that we’ve separated checks, account numbers, and cards, let’s look at how these details show up in everyday transactions.

1. Direct Deposit

When a job or government payment hits your account, it uses:

- Routing number – identifies your bank

- Account number – identifies your specific account

Your debit card isn’t part of the process at all.

2. Automatic Bill Payments

If you pay through your bank?

The system uses your account and routing numbers.

If you pay through a company’s website?

It might use your debit card.

3. Writing a Check

A check pulls money from your bank account, not your debit card.

The routing and account number on check provide instructions to the banking system.

4. Using a Debit Card at a Store

Your card number and PIN authorize the transaction.

The money comes straight from your account balance.

5. Online Purchases

When you enter your card number online, you’re authorizing a debit card transaction—not giving away direct access to your account.

Your actual account number stays private.

6. ACH Transfers

Payments like rent, utilities, or bank-to-bank transfers usually rely on:

- routing number

- account number

This method skips cards entirely.

Security: What You Should (and Shouldn’t) Share

This is where understanding your bank details becomes extremely important.

Safe to Share When Needed:

- routing number

- account number (only with trusted parties)

- debit card number (with legitimate merchants)

Never Share:

- your PIN

- online banking password

- one-time codes sent via text

- your full account details through email or text

- private information over the phone unless you initiated the call with a verified number.

A good rule:

If someone pressures you to share information quickly, pause. Real institutions don’t rush you.

Tips for Keeping Your Banking Info Safe

You don’t need to be paranoid—just aware. A few simple habits go a long way:

- Don’t save your card info everywhere online

- Shred old documents with banking details

- Use your bank’s official app instead of email for communication

- Set up transaction alerts

- Review your statements monthly

- Lock your debit card temporarily if you misplace it

Small habits build strong protection for your money.

The Big Picture: Why Understanding Bank Details Helps You Move Confidently

You don’t need to memorize every technical term. But knowing the essentials—like where to find your account number on check or the real debit card definition—gives you confidence when handling money.

It helps you:

- avoid mistakes

- recognize suspicious activity

- complete payments without confusion

- talk to financial institutions without second-guessing yourself

Money becomes a lot less stressful when you understand how it moves.

Final Thoughts

Bank details aren’t just numbers. They’re the foundation of almost every payment you make. Once you understand how they all connect—your account, your routing number, your card, your checks—everything suddenly feels simpler.

And once it feels simple, it becomes manageable. And once it’s manageable, you’re in control.