Why the First 24 Hours After Roof Damage Can Decide an Insurance Claim

After a major storm, most homeowners follow their instincts. They head outside to clear fallen branches from the driveway, check on the fences, and look for shingles that might have blown off. This makes sense because the mess is the most urgent thing to fix. However, when it comes to insurance, what feels urgent is not always what is most important. Your insurance claim is built on a foundation of timelines, records, and decisions made long before anyone ever climbs a ladder to start repairs.

In many cases, the first 24 hours after your roof is damaged can determine whether your claim moves along smoothly or gets stuck in a lengthy dispute with the insurance company. This is not because insurers expect you to be a roofing expert. It is because storms create “messy” evidence. Wind-driven rain dries up. Debris gets moved. Temporary patches change the roof’s appearance. A claim is often won or lost based on whether an adjuster can clearly see the link between a specific storm and the damage to your home. The first day is when it is easiest to prove that link, giving you confidence that you are taking the right steps.

The Insurance Clock: Why Timing is Everything

Homeowners are often shocked to learn how much their insurance depends on the clock. You might think that if a storm happened and your roof is now leaking, the insurance company will simply pay. In reality, insurers look at “causation.” They want to know two things: whether the storm caused the damage and whether you did your part to prevent it from getting worse. Most policies have a rule that you must give “prompt notice” and take “reasonable care” to protect your property after a loss.

If water keeps leaking into your home for several days because you didn’t cover a hole, the insurance company might refuse to pay for the ruined drywall or moldy carpet. They may argue that the interior damage happened because you waited too long to act. By documenting everything in the first 24 hours, you prevent these “gray areas” from hurting your claim. Even if a professional adjuster cannot get to your house for a week because they are busy, your personal record from day one keeps the facts straight.

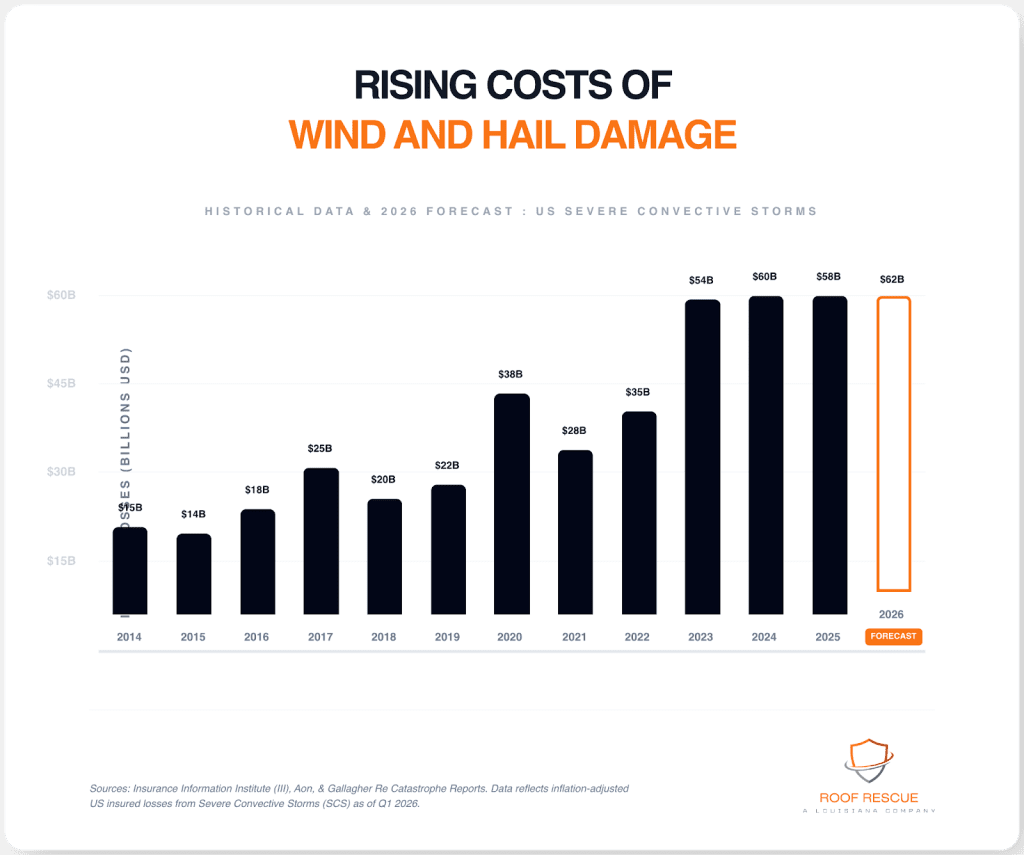

According to data from the Insurance Information Institute, the cost of property damage from wind and hail has risen significantly over the last decade. This makes insurance companies much more careful about the details. Reporting the loss early sets the “official clock” and helps you avoid confusion if another storm hits the area a few days later. When two storms happen close together, insurers often argue about which one caused the problem. An early report anchors your claim to a specific date.

Documentation: Turning Photos into Evidence

The most valuable thing you can do in the first few hours is very simple: take pictures and videos. Do not think of this as busywork; think of it as collecting evidence for a court case. Start from the ground in a safe spot and take wide shots of the whole house. Then, get close-ups of any visible damage. If you see shingles in the yard, photograph them where they landed. If a tree limb hit the roof, take a picture of the impact point.

After you finish outside, go inside and look for signs of water. Take photos of:

- Water stains on the ceiling.

- Damp spots on the drywall.

- Wet insulation in the attic.

- Water trails near vents or your chimney.

The goal is to capture the home exactly as it looked right after the storm. As soon as you put up a tarp or move debris, the evidence changes. A simple set of photos taken early can prevent a later debate over whether the damage was new or pre-existing.

Keep a Paper Trail

Writing things down is just as important as taking pictures. Note the exact date and time the storm hit. Keep a log of every phone call you make to the insurance company. Write down the claim number, the names of the people you spoke with, and any reference IDs they give you. These details might feel small now, but they are a lifesaver if your claim takes weeks to process and you have to talk to five different representatives, helping you feel organized and in control.

Safety and the Danger of the DIY Inspection

One of the biggest mistakes homeowners make is climbing onto the roof to see the damage for themselves. It is natural to want answers, but walking on a storm-damaged roof is incredibly dangerous. Shingles can be loose, the wood underneath could be weak, and there might even be downed power lines touching the house that you can’t see. Beyond the physical danger, walking on the roof can cause additional damage, such as breaking shingle seals that were still intact. This can prompt the insurance adjuster to question what was caused by the storm and what was caused by your walking around, so knowing how to stay safe can help you feel more secure in managing the situation.

For a detailed look at how to handle these moments safely, you can refer to this guide on what to do immediately after storm roof damage in Zachary, Louisiana. It provides a step-by-step approach to gathering evidence without putting yourself at risk. Remember, ground-level photos and interior checks are usually sufficient to initiate the claim. Let a licensed professional handle the high-altitude inspection, especially if you have safety concerns about walking on the roof.

Mitigation: Stopping the Damage Safely

Your insurance policy likely requires you to perform “mitigation.” This does not mean you have to fix the roof permanently right away. It means you must stop water from continuing to pour into your house. Placing a tarp over a hole or placing buckets under a leak are common mitigation measures. If you hire someone to install a tarp, ensure they are experienced and keep the receipt. Insurers will usually reimburse you for these emergency costs, but only if you have the paperwork to prove it.

Be careful not to over-mitigate. Do not rip off shingles to “look” for more damage, and do not let a contractor start a complete replacement before the insurance adjuster has seen the roof. If you change the roof too much, the insurer may say they didn’t have a fair chance to evaluate the original storm damage. Stabilize the situation, take photos, and wait for the official inspection before starting major repairs.

The Value of a Professional Inspection

Roof damage can be very sneaky. Wind can break the waterproof seals on your shingles without blowing them off. Hail can “bruise” the shingles, which you won’t see from the ground, but it will lead to a leak in six months. By the time the leak shows up, the insurance company might say it is too late to file a claim. A professional inspection soon after the storm can find these hidden issues.

A licensed roofer can provide a written report that explains exactly what is wrong. This report adds professional weight to your claim. As noted in a recent analysis on how Louisiana homeowners can protect their long-term property value, timely inspections are one of the best ways to avoid “delayed damage” surprises that can cost you thousands of dollars out of pocket later on.

Avoiding “Storm Chaser” Scams

After a storm, you might see contractors from out of town knocking on doors. Some are honest, but others are “storm chasers” who do quick, poor-quality work and then vanish. They might pressure you to sign a contract before you’ve even talked to your insurance company. Always ask for proof of local licensing and insurance. A reputable local contractor will be happy to explain their findings and work with your insurance timeline rather than rushing you into a deal that sounds too good to be true.

Building Your Claim-Friendly Record

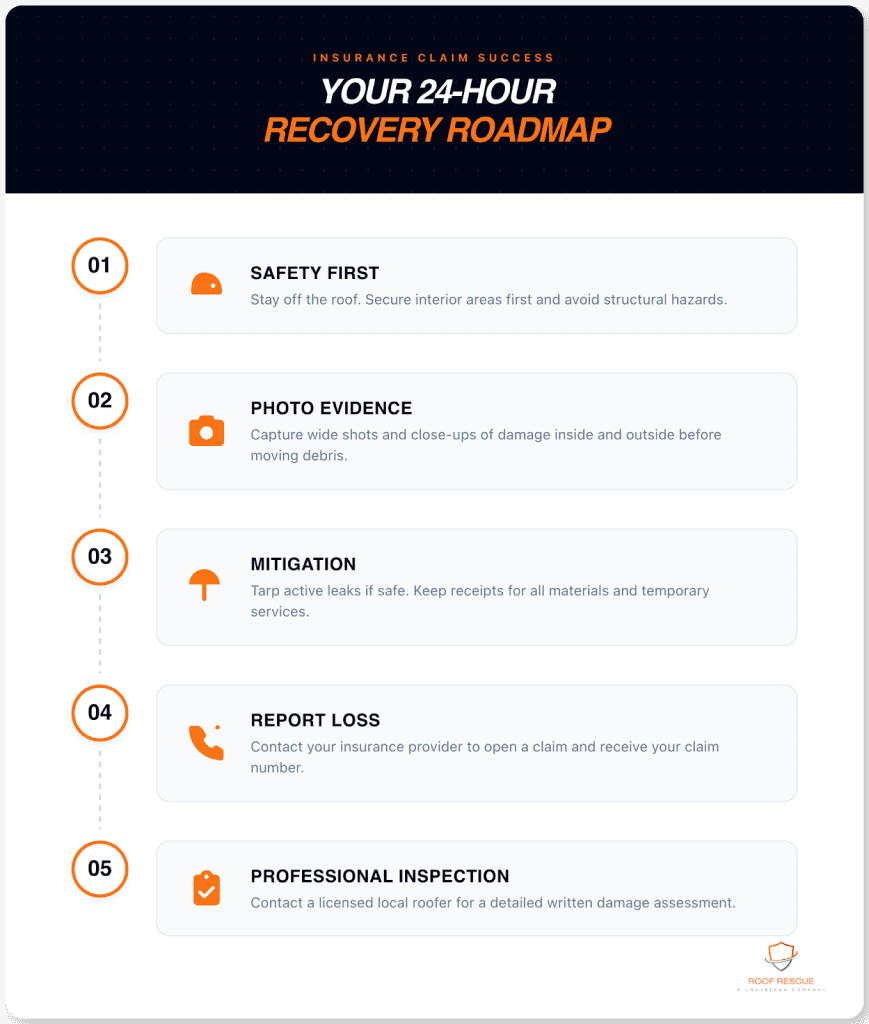

You don’t have to be perfect in those first 24 hours, but you do have to be organized. Follow this simple checklist to build a strong record:

- Safety First: Stay off the roof and watch for power lines.

- Document Everything: Take photos and videos of the outside and inside.

- Mitigate: Use tarps or buckets to stop water, and save your receipts.

- Report the Loss: Call your insurance company immediately to get a claim number.

- Schedule a Pro: Get a licensed local roofer to do a full inspection.

Following these steps doesn’t guarantee your claim will be approved, but it makes the process much more predictable and reduces the chance of a dispute. Studies from the Insurance Institute for Business & Home Safety show that homes with documented maintenance and quick storm responses are far less likely to suffer long-term structural failure.

Record-Keeping is the New Recovery

Today’s insurance market is tighter than it used to be. Insurers are reviewing maintenance records more closely and are more cautious about paying for damage that appears to be “wear and tear.” This means that as a homeowner, your job after a storm is no longer just cleanup—it is record-keeping. The first 24 hours are your best opportunity to capture the truth of what happened to your home. By taking a measured, documented approach, you protect your safety, your finances, and the future value of your property. The storm may be out of your control, but your recovery process is not.