NEW ORLEANS, Louisiana — Notary public demand across Louisiana is drawing renewed attention as the state prepares to implement a significant increase in the financial responsibility required of commissioned notaries. The shift, scheduled to take effect February 1, 2026, coincides with ongoing high volumes of notarized paperwork tied to real estate transactions, estate matters, and legal authorizations statewide.

Stricter Surety Bond Threshold Could Affect Notary Availability

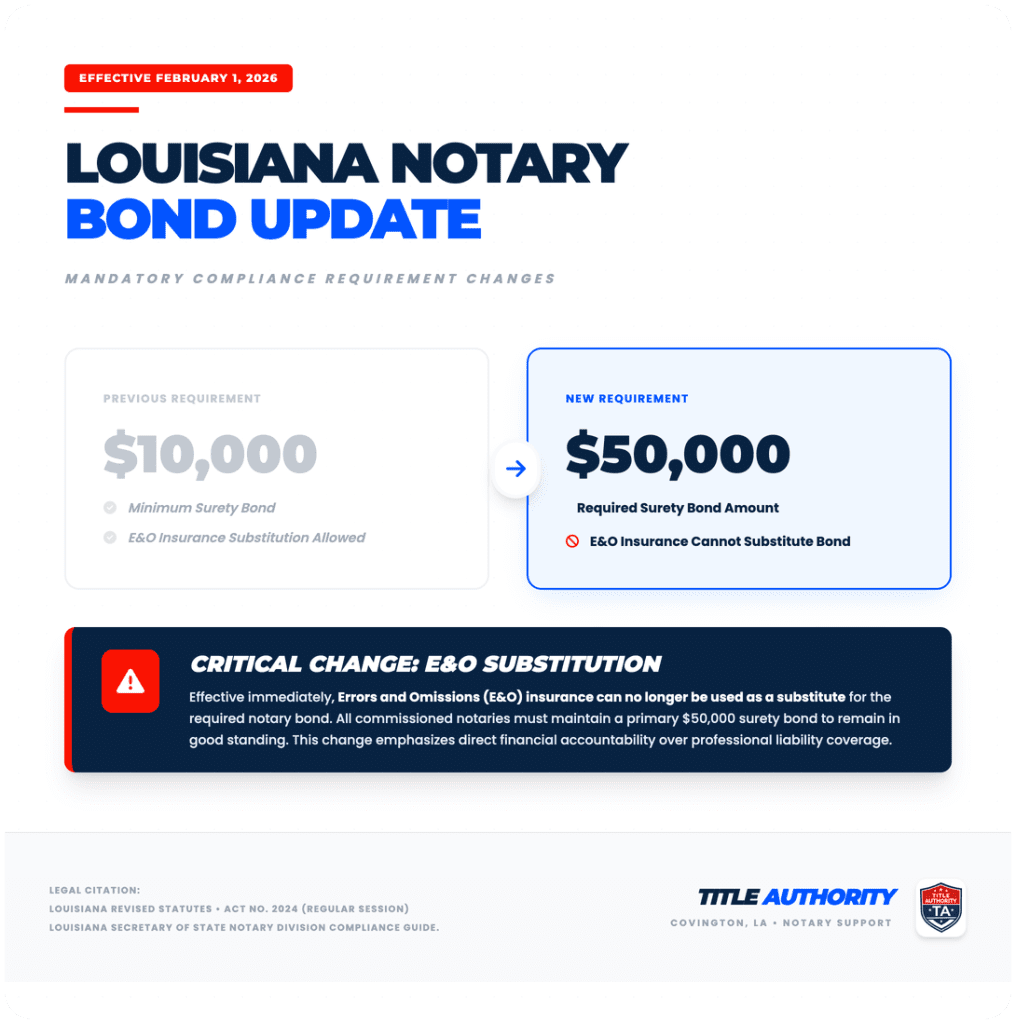

Under a new law passed by the Louisiana Legislature, all commissioned notaries will be required to carry a $50,000 surety bond, up from the previous $10,000 minimum. The legislation also eliminates the option of using errors and omissions insurance in place of a surety bond. By imposing this higher threshold, regulators aim to increase accountability for notarial acts and reduce liability risks tied to improperly executed documents. National Notary Association reporting on the requirement highlights the broad impact for both long-time and newly commissioned notaries.

Industry observers say the requirement could influence availability and workload, especially in markets like Greater New Orleans, where demand often spikes in alignment with real estate closing schedules.

Notary Roles in Louisiana Often Exceed Those in Other States

Louisiana is one of the few states where notaries public function under a civil-law tradition that grants them broader authority than in many common-law jurisdictions. According to national legal summaries, Louisiana notaries are commissioned by the governor and authorized to handle a range of civil-law matters, including conveyances, wills, partitions, and inventories. United States notary public data notes that Louisiana notaries can prepare and execute instruments that elsewhere would require legal counsel.

This broader scope is one reason why notarization remains central to major transactions, even as many administrative processes migrate online.

Real Estate Paperwork Drives a Large Share of Notarization Needs

Real property transfers remain among the most notarization-intensive categories in Louisiana. Authentic acts — formal notarial instruments that require execution before a notary and two witnesses — are commonly used to transfer immovable property and provide prima facie proof of the contents of a transaction. Under the Louisiana Civil Code, an authentic act is “a writing executed before a notary public…in the presence of two witnesses,” signaling heightened formal requirements for real estate and similar transactions. Louisiana Civil Code Article 1833

When real estate documents are signed improperly or without full witness presence, recording offices may reject filings, triggering delays that can extend closing schedules and burden buyers, sellers, and lenders alike.

Powers of Attorney and Sworn Statements Add to Notary Volume

Beyond property transactions, powers of attorney are another major driver of demand for notarization. Financial institutions, healthcare providers, and other authorities often require notarized powers of attorney to verify the principal’s identity and intent. If these documents are not executed in accordance with state requirements, they may be rejected, creating timing pressures, particularly in medical or emergency contexts.

Sworn affidavits are a common type of notarized document used in court filings, insurance claims, and administrative processes. Notarization adds a formal layer of identity verification to sworn statements, which agencies and courts rely upon when assessing credibility.

Succession, Estate, and Business Transactions Contribute to Workloads

Succession and estate-related documents often require notarization because they touch on asset distribution and authority delegation. Courts and financial institutions typically favor notarized execution to reduce disputes and confirm document validity.

Additionally, business transactions — such as corporate agreements, banking resolutions, and compliance filings — often require notarized signatures. In a fast-moving business environment, the absence of timely notarization can stall processes ranging from credit approvals to contract finalization.

Market Signals Point to Preparation as Key

Legal and industry analysts emphasize that most notarization failures stem from preventable issues, including missing pages, mismatches between document and identification names, and a lack of required witnesses. Awareness of these requirements can reduce repeat appointments and accelerate processing timelines.

For a broader explanation of how Louisiana notarization differs from other states, why access and timing matter in markets like New Orleans, and what consumers should prepare before signing, see the Origin analysis: Louisiana notary public requirements in New Orleans and what to prepare before you sign.

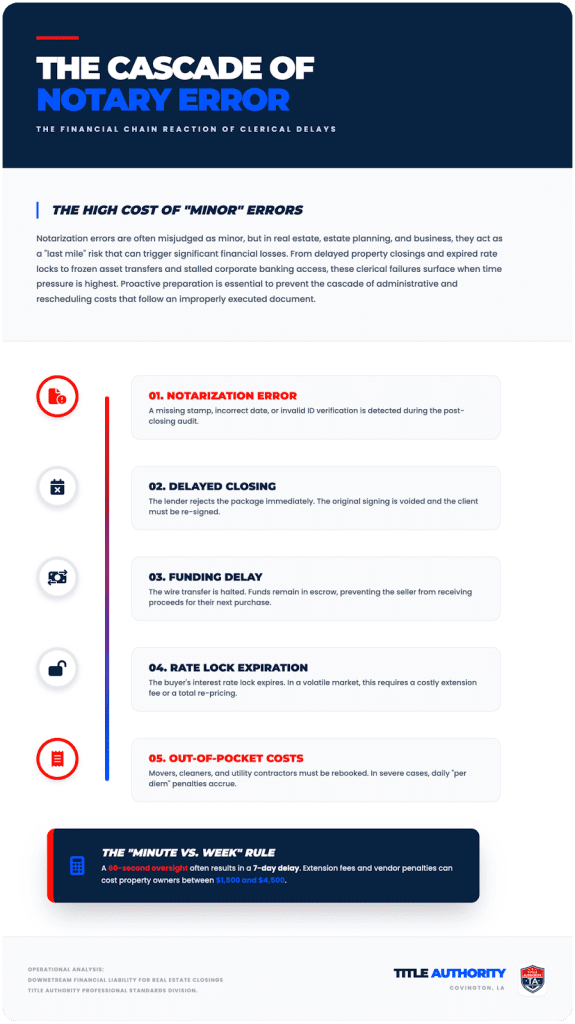

Transaction Delays Often Carry Downstream Financial Consequences

While notarization errors are often viewed as minor administrative setbacks, their downstream effects can be significant. In real estate transactions, a single improperly executed document can delay funding, postpone recordation, or require the parties to reconvene to execute additional documents. Those delays can trigger rate lock extensions, rescheduling fees, or contractual penalties, particularly when transactions are already operating on compressed timelines.

Legal professionals note that similar ripple effects appear in estate and succession matters. When notarized filings are rejected by courts or financial institutions, asset transfers may be frozen until corrected documents are submitted. In business settings, rejected notarized resolutions or authorizations can stall banking access, financing approvals, or regulatory compliance reviews, extending timelines well beyond initial expectations.

Because notarization often sits near the end of a transaction workflow, failures tend to surface when time pressure is highest. Analysts describe notarization as a “last mile” risk in legal and financial processes, where earlier preparation can prevent disproportionate delays later. As compliance standards tighten and transaction volumes remain elevated, the cost of even small execution errors becomes more visible.

Outlook for 2026 and Beyond

As Louisiana moves toward the 2026 implementation of the $50,000 bond requirement, legal service providers and notaries alike are adjusting to the regulatory shift. The change reflects broader trends in risk management and public accountability in notarial acts, while reinforcing the continued importance of notarization in high-stakes legal and financial contexts.

In practice, real estate professionals, estate planners, and consumers should plan for increased demand, maintain detailed preparation checklists, and engage experienced notaries early in transaction workflows to avoid disruptions as the new standards take effect.