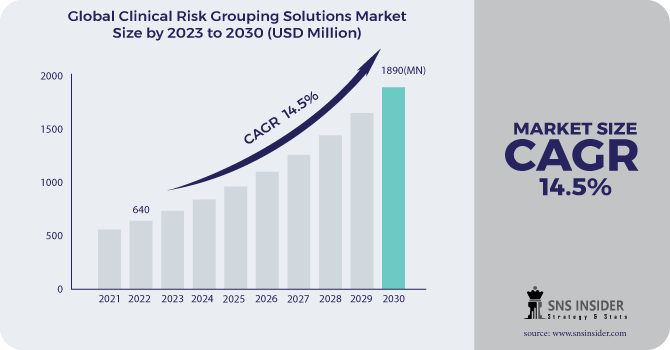

The global Clinical Risk Grouping Solutions market size valued at USD 640 million in 2022 and projected to reach USD 1,890 million by 2030. This significant expansion, driven by a compound annual growth rate (CAGR) of 14.5%, underscores the increasing adoption and importance of clinical risk grouping solutions in the healthcare industry.

Key Market Drivers

Several factors contribute to the robust growth of the Clinical Risk Grouping Solutions market:

- Rising Healthcare Expenditures: Increasing healthcare costs globally have necessitated the adoption of efficient risk management solutions to optimize patient care and resource allocation.

- Growing Prevalence of Chronic Diseases: The surge in chronic diseases such as diabetes, cardiovascular diseases, and cancer has driven the demand for advanced clinical risk assessment tools to improve patient outcomes and manage healthcare costs.

- Technological Advancements: Innovations in artificial intelligence (AI) and machine learning (ML) have significantly enhanced the capabilities of clinical risk grouping solutions, providing more accurate and actionable insights.

- Regulatory Requirements: Stringent regulations and guidelines for patient data management and risk assessment have accelerated the adoption of clinical risk grouping solutions across healthcare institutions.

Get a Free Sample Report of Clinical Risk Grouping Solutions Market: https://www.snsinsider.com/sample-request/2027

Market Segmentation

The Clinical Risk Grouping Solutions market is segmented based on product type, application, end-user, and region.

- By Product Type: The market includes software solutions, services, and hardware components. Software solutions hold the largest market share due to their widespread application in healthcare analytics and risk management.

- By Application: The primary applications of clinical risk grouping solutions include population health management, clinical decision support, financial management, and performance measurement.

- By End-User: Major end-users are hospitals, healthcare payers, and ambulatory care centers. Hospitals dominate the market due to the high volume of patient data they manage and the need for efficient risk assessment tools.

- By Region: The market is analyzed across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America leads the market, driven by advanced healthcare infrastructure and high healthcare expenditures. However, the Asia-Pacific region is expected to witness the highest growth rate due to increasing healthcare investments and technological adoption.

Competitive Landscape

The Clinical Risk Grouping Solutions market is highly competitive, with several key players striving to enhance their market presence through product innovations, strategic collaborations, and mergers and acquisitions. Notable companies in the market include:

- 3M Health Information Systems: A leading player offering comprehensive clinical risk grouping solutions with advanced analytics capabilities.

- Optum, Inc.: Known for its robust data analytics and risk assessment tools, Optum continues to expand its market reach through strategic partnerships.

- Cerner Corporation: A major player providing integrated clinical risk management solutions, Cerner focuses on enhancing patient care through innovative technologies.

- Johns Hopkins ACG System: Renowned for its sophisticated risk adjustment and predictive modeling solutions, Johns Hopkins ACG System is a key contributor to the market.

Future Outlook

The future of the Clinical Risk Grouping Solutions market looks promising, with continued advancements in technology and increasing awareness about the importance of risk management in healthcare. The integration of AI and ML in clinical risk assessment tools is expected to revolutionize the market, providing more precise and personalized risk stratification.

Moreover, the ongoing COVID-19 pandemic has highlighted the critical need for efficient risk management solutions in healthcare, further driving market growth. As healthcare providers and payers continue to prioritize patient safety and cost-efficiency, the demand for clinical risk grouping solutions is anticipated to rise significantly.

Conclusion

The Clinical Risk Grouping Solutions market is set for substantial growth, driven by rising healthcare expenditures, increasing prevalence of chronic diseases, technological advancements, and stringent regulatory requirements. With a projected CAGR of 14.5% from 2023 to 2030, the market is expected to reach USD 1,890 million by 2030, offering lucrative opportunities for key players and new entrants alike.

As the healthcare landscape continues to evolve, the adoption of advanced clinical risk grouping solutions will play a pivotal role in optimizing patient care, improving outcomes, and managing healthcare costs effectively.

Other Reports You May Like:

Life Science Analytics Market Size

Orthopedic Software Market Size

Patient Access Solutions Market Size